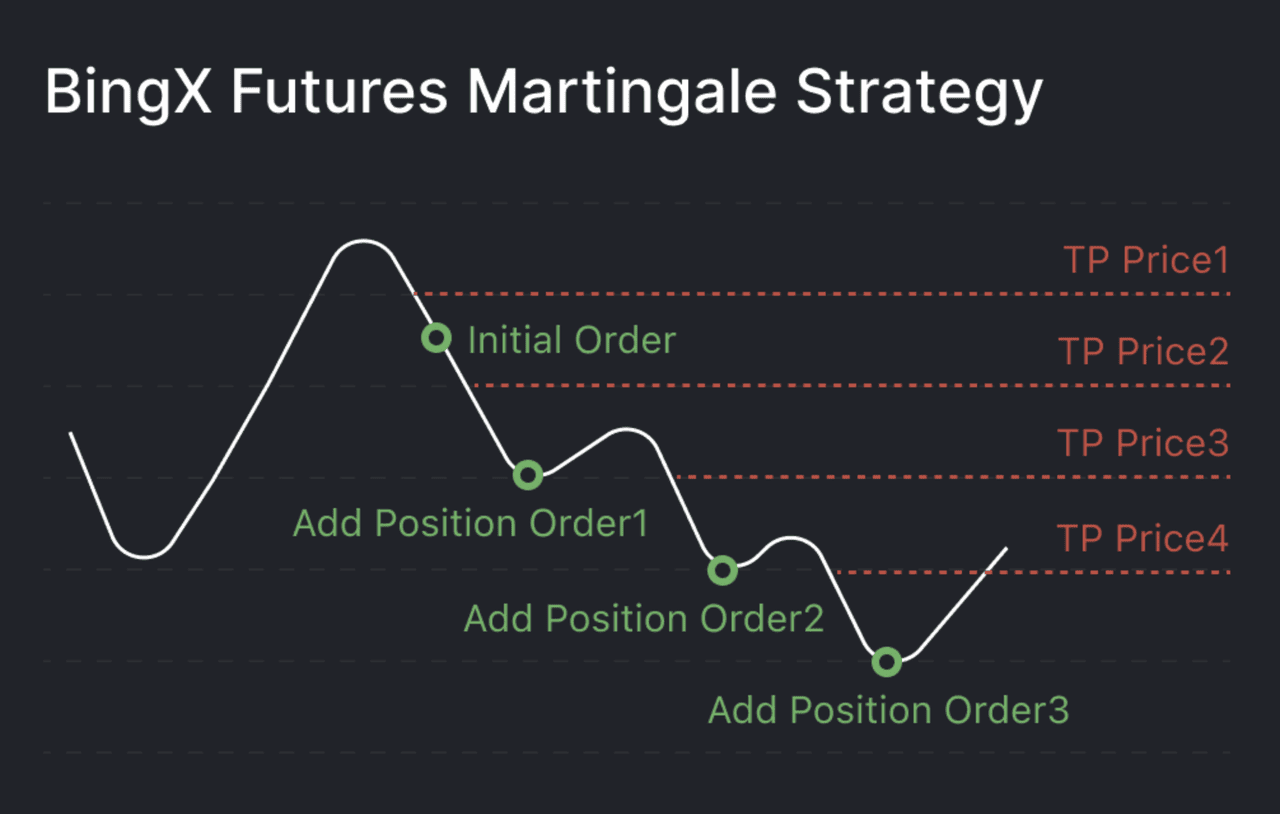

Preparation Before Using the Martingale Strategy

The practical focus of the Martingale strategy is not simply adding positions after losses, but first confirming account capital, trading instruments, leverage ratio, pip value, maximum layers, and exit conditions. If these parameters are not written into the trading plan in advance, the strategy can easily turn into disorderly position adding during consecutive adverse market conditions.

In forex and contract for difference trading, contracts for difference, officially known as Contract for Difference and abbreviated asCFD, usually use a margin system. Margin trading allows traders to control larger notional positions with part of their funds, but it also causes losses to change according to the notional position. Each Martingale position increase raises notional risk, so it needs to be managed with numbers rather than subjective judgment.

Six Parameters to Define Before Practical Use

Initial lot size, such as 0.01 lot, 0.02 lot, or 0.10 lot.

Position-increase multiplier, such as 1.3 times, 1.5 times, or 2 times.

Maximum number of position-increase layers, such as 3 layers, 4 layers, or 5 layers.

Maximum loss per trade group, such as 3% to 8% of account equity.

Position-increase trigger distance, such as every 50 pips, 100 pips, or based on volatility.

Forced stop conditions, such as reaching the daily loss limit, weekly loss limit, or lower margin-level threshold.

| Setting Item | Key Parameter | Applicable Scenario | Main Risk |

|---|---|---|---|

| Initial lot size | Commonly tested from 0.01 lot | Small accounts, demo accounts, and process verification | An initial lot size that is too large will compress the room for later position increases |

| Position-increase multiplier | 1.3 times to 2 times is relatively common | Conservative testing or traditional escalation models | The higher the multiplier, the faster margin requirements grow |

| Maximum layers | Usually limited in advance to 3 to 5 layers | Preventing consecutive position increases from getting out of control | Too many layers may approach the capital limit |

| Total risk limit | May be set at 3% to 8% of account equity | Risk budget for a single strategy group | Continuing to trade after exceeding the limit will undermine discipline |

How to Design a Martingale Trading Process

Step 1: Select a Suitable Market Environment for Testing

Martingale relies more on prices returning near the mean, so using it in a clear one-way trend carries higher risk. Traders may first observe whether the market is in range-bound movement, low-volatility consolidation, or a high-liquidity trading session. If prices continue to make new highs or new lows, and moving averages, volatility, and trading structure all indicate trend continuation, the risk of adding positions after losses will increase significantly.

Average True Range, officially known as Average True Range and abbreviated asATR, can be used as a tool for observing volatility ranges. If the 14-period ATR of an instrument expands significantly, it indicates that recent price volatility has increased, and the position-increase spacing and stop-loss distance also need to be adjusted accordingly. ATR is not a directional indicator; it only helps estimate the size of price fluctuations.

Step 2: Set the Initial Position

The initial position should be calculated backward from account equity and maximum risk rather than determined by personal preference. For example, if account equity is USD 1,000 and the maximum acceptable loss per group is set at 5%, then the loss limit per group is USD 50. If the plan allows up to 4 position-increase layers, traders need to estimate in advance whether the combined loss of each layer under adverse price movement will exceed USD 50.

Step 3: Calculate Margin Usage

The margin formula is: required margin equals notional principal divided by the leverage multiple. If the notional size of 0.10 lot of a major currency pair is about 10,000 base currency units and leverage is 1:100, the margin is approximately the equivalent of 100 base currency units. If positions are increased to 0.20 lot, 0.40 lot, and 0.80 lot, margin usage will increase in line with the notional position.

Determine account equity, such as USD 1,000 or USD 5,000.

Determine the maximum risk percentage, such as 3%, 5%, or 8%.

Determine the initial lot size, such as 0.01 lot.

Determine the position-increase multiplier, such as 1.5 times or 2 times.

List the lot size, margin, and possible loss for each layer.

Check whether the worst-case scenario would trigger stop-out or breach the risk limit.

| Layer | Key Parameter | Applicable Scenario | Main Risk |

|---|---|---|---|

| Layer 1 | 0.01 lot, used as the initial exploratory position | Strategy launch and market observation | Incorrect directional judgment will trigger the subsequent plan |

| Layer 2 | 0.02 lot, increased by 2 times | Planned position increase after a short-term pullback | Total position rises to 0.03 lot |

| Layer 3 | 0.04 lot, continuing to increase by 2 times | Stress testing when the range has not broken down | Total position rises to 0.07 lot |

| Layer 4 | 0.08 lot, reaching the preset limit | Final planned layer handling | If adverse movement continues, exit rules should be executed |

How to Set Position-Increase Distance and Exit Rules

Position-increase distance cannot be determined only by a fixed number of pips. Pip value, volatility, and trading sessions vary greatly across instruments. Major currency pairs may have lower spreads during normal liquidity periods, while gold, crude oil, indices, and crypto-asset CFDs may have larger price fluctuations. If the same 50-pip position-increase distance is used for all instruments, the risk of high-volatility instruments can easily be underestimated.

A more robust approach is to combine position-increase distance with volatility. For example, traders may use 0.5 times to 1 time ATR as a reference range, or set the distance based on the average volatility over the past 20 trading days. Whichever method is used, the maximum number of layers and total loss limit should be set in advance.

Position-increase distance may refer to 0.5 times to 1 time ATR, but it needs to be combined with spreads and instrument characteristics.

Each trade group should have a maximum floating loss amount, which should not be temporarily expanded due to emotions during trading.

After reaching the maximum number of layers, no further positions should be added.

If price breaks through the range boundary and forms a trend, exit or position-reduction rules should be executed.

Around major economic data releases, starting new Martingale groups may be paused.

Strategy Handling Under Different Market Conditions

Range-Bound Market Environment

A range-bound market environment is a relatively easier scenario for testing Martingale because the mean-reversion assumption is more likely to appear when prices move repeatedly between upper and lower boundaries. Even within a range, however, traders still need to confirm whether the boundaries remain valid. If price breaks the range with strong volume and continues, the original mean may become invalid.

Trending Market Environment

In trending markets, traditional Martingale carries higher risk. Whether price continues rising in an uptrend or continues falling in a downtrend, adding against the direction of losses may cause losses to accumulate continuously. At this point, it may be more appropriate to consider fixed risk percentages, trend following, or Reverse Martingale methods rather than continuously increasing positions in the losing direction.

High-Volatility Event Environment

Around interest rate decisions, inflation data, employment data, central bank speeches, earnings releases, and geopolitical events, quotes may move rapidly. Wider spreads, increased slippage, and pending-order execution prices deviating from expectations are more common in these conditions. Martingale may not be executed at planned prices in this type of environment.

| Market Environment | Key Parameter | Applicable Scenario | Main Risk |

|---|---|---|---|

| Low-volatility range | Narrower position-increase spacing and lower initial lot size | Demo testing and rule verification | Risk changes rapidly after a range breakout |

| Trend continuation | Reduce counter-trend position increases and control total risk | Trend-following strategies or observation periods | Traditional Martingale is prone to consecutive losses |

| Major data period | Increase the risk buffer or pause trading | High-volatility event management | Slippage and spread widening affect execution |

| Low-liquidity period | Reduce lot size and number of layers | Overnight periods, holidays, or less popular instruments | Quote jumps and insufficient market depth |

Demo Account Testing Process

Before entering a real-money environment, the Martingale strategy should first be tested on a demo account. The testing goal is not to see whether a single trade is profitable, but to evaluate consecutive losses, maximum drawdown, margin level, and execution deviation. At least 30 to 100 groups of trade samples should be recorded, covering different market conditions.

Create a testing spreadsheet to record the instrument, time, direction, lot size, spread, and number of position-increase layers.

Set a maximum loss amount and maximum number of layers for each trade group.

Record the total position and margin level after each position increase.

Calculate the maximum number of consecutive losses, maximum floating loss, and maximum drawdown.

Compare the risk differences among different multipliers, such as 1.3 times, 1.5 times, and 2 times.

Check the strategy’s performance in trending markets, range-bound markets, and high-volatility markets.

If the demo results rely on excessively high layers or excessively high leverage, the parameters should be reduced or live-account migration should be stopped.

Risk Management Framework in a Live Account

If traders observe the Martingale strategy in a live account, it should be kept within a risk budget. A live account is affected by funding pressure, slippage, spreads, platform execution, and emotions. Any temporary increase in layers, removal of loss limits, or rise in the multiplier will change the originally tested strategy structure.

The maximum loss per trade group may be limited to 3% to 5% of account equity.

The maximum daily loss may be limited to within 5% of account equity.

After 2 to 3 consecutive losing groups, trading may be paused and market conditions reviewed.

When the margin level falls below 200%, the total position should be reassessed.

The same position-increase model should not be used simultaneously across multiple highly correlated instruments.

All parameter changes should first return to demo account testing.

The practical value of the Martingale strategy lies in helping traders understand the relationship between position escalation and capital constraints, rather than providing certain outcomes. Only when maximum loss, maximum layers, instrument selection, and exit rules can all be quantified does it have a basis for evaluation.

Martingale Strategy FAQs

How should the initial lot size of a Martingale strategy be estimated?

The initial lot size should be calculated backward from account equity, maximum loss per group, maximum layers, and the instrument’s pip value. If the initial lot size is too large, the room for later position increases will be significantly reduced, and stop-out risk will also rise.

Is it necessary to set the position-increase multiplier at 2 times?

No. A 2-times multiplier is the traditional form, but in practice, 1.3 times or 1.5 times may also be tested. The lower the multiplier, the larger the market move may be needed to recover losses, but margin pressure is usually lower.

In what market conditions is the Martingale strategy suitable for testing?

It is more commonly tested under range-bound and mean-reversion assumptions. If the market is in a clear one-way trend, high-volatility event period, or low-liquidity session, strategy risk will increase significantly.

Why is stress testing needed before using it in a live account?

Stress testing can show how consecutive losses, spread widening, slippage, and declining margin levels affect the account. Without stress testing, it is difficult for traders to judge whether the maximum number of layers matches the capital size.